by Emily Michels, Health Policy Fellow

You’ve spent hours poring over insurance plan premiums, or perhaps worked with a health coverage guide to find what health plan works best for you, and now you get to see that choice in action. When you’re sick or hurt, the last things on your mind are likely the intricacies of your health plan’s in and out-of-network policies. You think your insurance company will cover all but your expected costs, but the enormous bill you receive afterwards from an out-of-network provider says otherwise…

Unfortunately, this scenario is very relatable for many Americans. In fact, according to a recent Consumer’s Union study, nearly one-third of privately-insured Americans have received a balance bill in the past two years. A balance bill, or “surprise medical bill,” is a charge attributed to the consumer for the difference between what his or her insurer pays to the provider and what the provider charges for the services – the leftover money owed. If the provider is in-network, the consumer will only need to pay the expected amount for that service. The “surprise” factor comes when the provider is unexpectedly out of one’s network, and patients are asked for much larger sums.

The following three scenarios are situations in which a consumer could receive a balance bill:

- The consumer makes an informed decision to use an out-of-network provider.

In this case, the consumer knows that he or she will be required to pay either the entire bill, or a higher cost sharing rate depending on his or her plan. Consumers may seek out a specific out-of-network provider they wish to complete a procedure, however this situation is not considered surprise billing and will not result in reimbursement, as the consumer expects the extra charges.

- The consumer is in an emergency medical situation.

The consumer may be taken to an out-of-network facility in an emergency. And, even if the consumer goes to an in-network hospital, there is no guarantee the providers will be in-network and charge the associated rates.

- The consumer receives care from an out-of-network provider at an in-network facility.

In non-emergency settings, the consumer often has the ability to select an in-network facility and provider for a procedure. The trouble, however, is with additional services that occur during the treatment. Though the main provider may be in-network, the anesthesiologist or surgical assistant, for example, may not be and can therefore charge large balance bills.

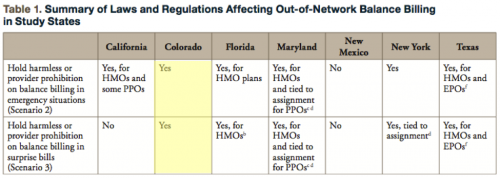

Although Colorado law provides protections for consumers in the case of scenarios two and three, many consumers don’t know about these protections. A recent Georgetown University report examined seven state approaches to balance billing, including Colorado’s. In Colorado,, health plans are required to hold patients harmless when treated by out-of-network providers at an in-network setting or in emergency situations, as long as the services would normally be covered. The problem, therefore, lies in the fact that the law does not prohibit providers from issuing these bills to consumers, and consumers unwittingly pay for them anyway.

Consumers often end up paying balance bills simply because they think that they will be sent to collection if they don’t. The next step in protecting Colorado consumers is to provide more notice and timely disclosure about their rights regarding balance bill payments. Once consumers know the right questions to ask and the opportunities for financial protection offered ahead of time, much of the confusion surrounding hefty balance bills could become a thing of the past.